11 March 2022

- Gartner client? Log in for personalized search results.

What is Ahead for Semiconductor Shortages

Contributor: KC Quah

Things are looking up, but recovery will take time.

In short:

- Any organisation that relies on semiconductor integrated circuits has been constrained since the beginning of 2021.

- The Gartner Index of Inventory Semiconductor Supply Chain Tracking (GIISST) provides insight into whether this will change—and when.

- Based on the data, organisations should consider certain short- and long-term tactics to mitigate disruption.

In February, we welcomed the Year of the Water Tiger, according to the traditional Chinese calendar. But what will the months ahead bring? Some would like to think that the tiger embodies courage, resilience and strength—all of which would be helpful during a time of struggle and disruption. The model for semiconductor inventory indicates that 2022 will be a year of recovery in which, for the most part, supply will start to catch up to demand.

The reality today is that any organisation, regardless of industry, that relies on semiconductor integrated circuits and the related components is now constrained—and has been since the beginning of 2021. So far as whether this continues, one key indicator to watch is the Gartner Index of Inventory Semiconductor Supply Chain Tracking (GIISST), which provides an aggregate level—or inventory position—as an indication of what is to come.

Download now: 3 Strategic Actions Supply Chain Leaders Must Take

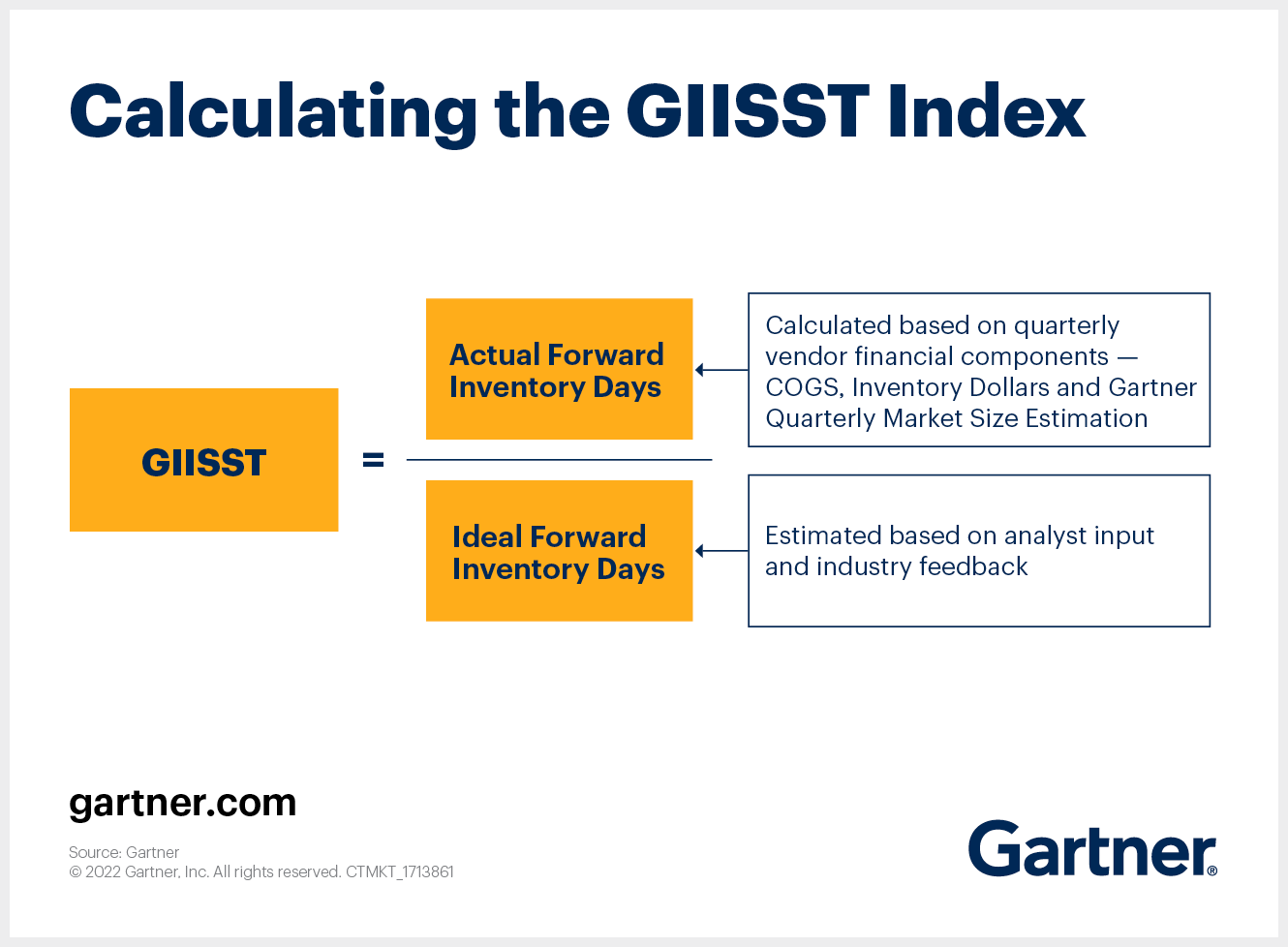

Before we dive into how the indicator is trending, let’s look at how it is defined and derived. The indicator considers the total value of inventory, i.e., raw materials, work in progress and finished goods. This inventory is derived from a list of about 200 publicly traded foundries, chip vendors, distributors, electronics manufacturing service (EMS) companies/contract electronics manufacturers (CEMs) and original equipment manufacturers (OEMs). From this, there is a calculation of actual forward days of inventory and ideal forward days of inventory.

Getting the GIIST

If the index is at 1.0 to 1.1, then the inventory is considered in balance and in a normal range. The farther the GIISST index is below 1.0, the more acute the shortage of inventory will be. The farther it is above 1.0, the more surplus of inventory you can expect.

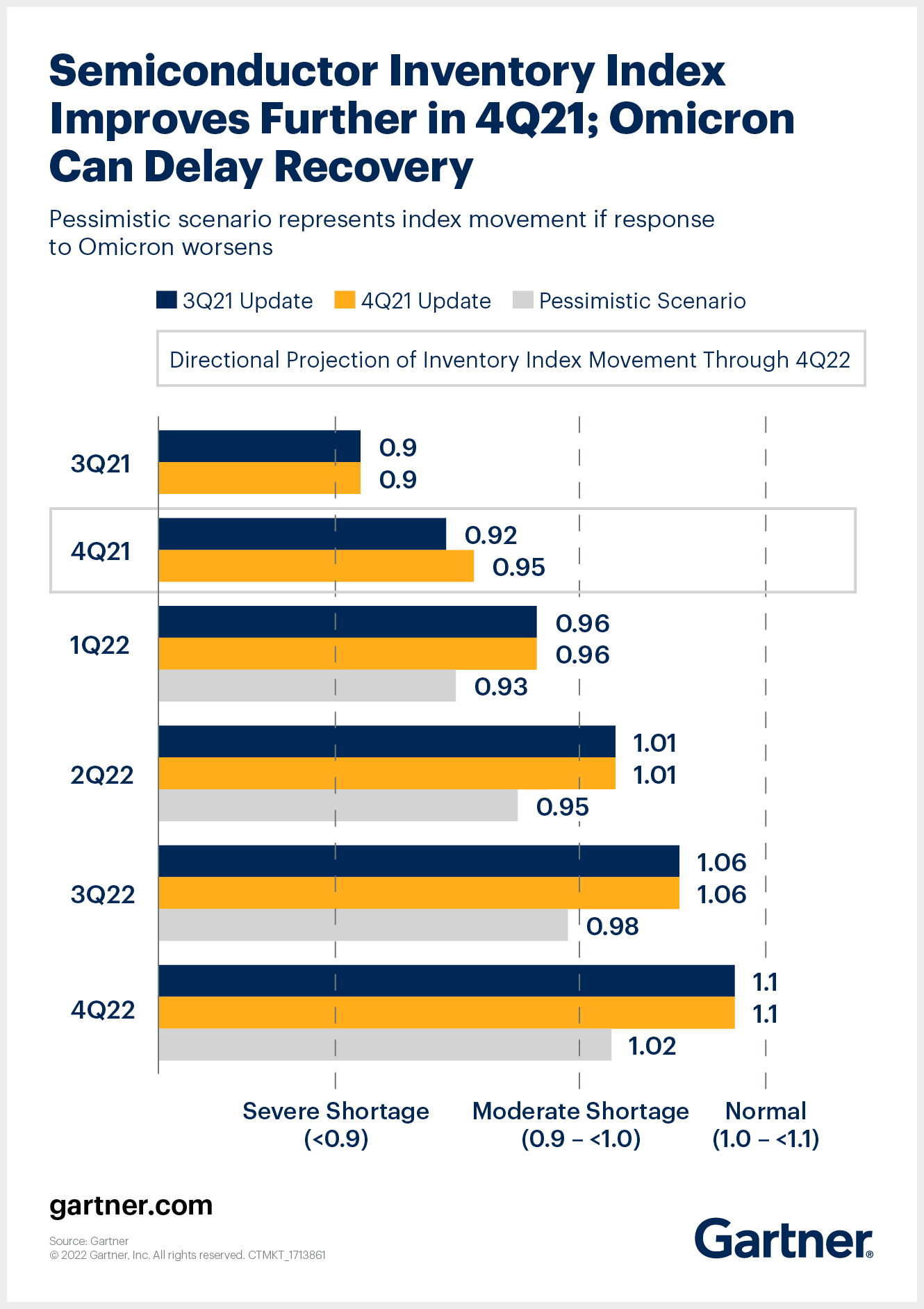

The latest update available is based on Q4 2021 data. You will see dark blue bars, which show the projection run with Q3 2021 data. The light blue bars use Q4 2021 data, and the green bars are the worst-case scenario—that is, if COVID-19 variants or geopolitical activities drive disruptions to production, as well as the movement of goods and people.

Based on the aggregated projection recovery, a return to normal inventory levels will not happen until Q3 or Q4 of this year. To be clear, this is an aggregated view and must be considered with some nuances. First, there is the pessimistic scenario, which while perhaps less likely, cannot be dismissed.

Second, we must look at the recovery of mature semiconductor process technologies separate from advanced technologies. The majority of the constrained mature semiconductor technology nodes are between 28 nm to 90 nm. The constraint here is semiconductor manufacturing capacity worldwide, and that is expected to recover by the end of 2022. The advanced nodes that are 10 nm and smaller, however, are constrained by advanced packaging, specifically Ajinomoto Build-up Film (ABF) substrates. With current lead times of anywhere from 52 to 70 weeks, that means that recovery would not occur until Q1 or Q2 of 2023.

What should companies do?

There are a limited number of levers in this situation. In the short term, the main tactics are paying a premium or using distributors and brokers to help obtain supply. Beyond this, companies should seek to understand where their exposure is in the high-tech ecosystem, going several tiers down if possible. The goal is to get better visibility and potentially establish more binding relationships for the future. In the longer term, strategies include redesigning products to use more common components, reducing the number of components used and potentially moving to programmable logic ICs, so software can be used to differentiate. Ultimately, building strategic long-term relationships—whether based on scale or innovation (e.g. co-engineering)—is a strategy worth considering.

I will leave you with this final and positive thought: While 2021 was highly constrained, 2022 looks to be the beginning of a recovery. And 2023 will see demand and supply come into balance. The models show that 2024 will bring a surplus of capacity, where supply will exceed demand.

This story was originally published on the Gartner Blog Network.

Experience Supply Chain conferences

Join your peers for the unveiling of the latest insights at the Gartner conferences.

Recommended resources for Gartner clients*:

Semiconductor Forecast Database, Worldwide, 4Q21 Update

Forecast: Semiconductor Foundry Revenue, Supply and Demand, Worldwide, 4Q21 Update

Supply Chain Executive Report: The Future of Supply Chain 2022

*Note that some documents may not be available to all Gartner clients.